On 20 January 2025, the United States welcomed back a very familiar face to the Oval Office, Donald Trump. And with him came Elon Musk, making his political debut in a way only he could. Love it or loathe it, the spectacle has been impossible to ignore. But let’s set aside politics and focus on what really moves the needle for investors: the markets.

Since Inauguration Day, global markets, particularly the US, have experienced heightened volatility, with the S&P 500 down 3.91% year to date as of 14 March 2025. You read that right, down 3.91%, not exactly the market apocalypse some media pundits would have you believe.

That said, given all the noise and the sheer influence of the US economy, it is understandable that investors might wonder how to position themselves in case of a stock market correction. So, let’s dive into the weeds of the global economy, specifically the US, and break down why our current positioning, which diversifies based on market capitalisation, still makes sense.

Too much exposure in US Equities?

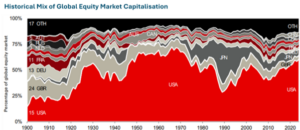

Investing in a global market cap portfolio means allocating to each region based on its share of the global equity market. At present, the US makes up approximately 64% of the global market. This is nothing new. As illustrated below, US-listed companies have long dominated global equity markets, with the red area highlighting their share over time. While US market concentration is currently elevated, history shows that global markets are dynamic, constantly adjusting as investors direct capital toward regions with the strongest expected returns. This is not unprecedented territory. It is simply the market doing what it has always done: adapting.

Source: UBS Global Investment Returns Yearbook: Summary Edition 2024 Elroy Dimson, Paul Marsh and Mike Staunton, DMS Database 2024 and FTSE Russell All-World Index Series weights (recent years).

While US market concentration may seem high, a closer look at its largest companies tells a more nuanced story. Conversations often focus on the influence of the Magnificent Seven: Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla, which now account for approximately 25%[1] of the US stock market. This level of concentration in US companies raises concerns about excessive concentration risk. But before we sound the alarm, let’s ask a fundamental question. Are these truly just “US” companies?

The answer to this question lies in where they generate their revenue, not just where they are listed. As shown in the chart below, more than 50% of the Magnificent Seven’s revenue, on average, comes from outside the US. This is a crucial detail often overlooked by those predicting America’s decline.

Amazon is the most domestically concentrated, with 73% of its revenue coming from the US. Alphabet, Microsoft, Tesla, and Meta generate between 46% and 51% of their revenue domestically, meaning nearly half of their income comes from global markets. Nvidia, the world’s second-largest company by market capitalisation, stands out, with only 31% of its revenue coming from the US, highlighting its extensive international reach.

[1] As of January 1, 2025, the total market capitalisation of the U.S. stock market stands at $62.2 trillion. This value represents the combined market cap of all U.S.-based public companies listed on the New York Stock Exchange, Nasdaq, or the OTCQX U.S. Market. The Magnificent Seven had a combined market cap of £15.52 trillion as of 01/01/2025.

Source: Individual company financial reports, sourced from annual and quarterly filings. Data compiled from SEC filings, investor relations reports, and earnings statements. Financial reports accessed directly from company investor relations pages: Alphabet (Google) – abc.xyz/investor, Amazon – amazon.com/ir, Apple – investor.apple.com, Meta – investor.fb.com, Microsoft – microsoft.com/investor, Nvidia – investor.nvidia.com, Tesla – ir.tesla.com.

Source: Individual company financial reports, sourced from annual and quarterly filings. Data compiled from SEC filings, investor relations reports, and earnings statements. Financial reports accessed directly from company investor relations pages: Alphabet (Google) – abc.xyz/investor, Amazon – amazon.com/ir, Apple – investor.apple.com, Meta – investor.fb.com, Microsoft – microsoft.com/investor, Nvidia – investor.nvidia.com, Tesla – ir.tesla.com.

So, is investing in US equities purely a bet on the US? Absolutely not. These are global businesses operating in a global economy, and their revenues reflect their worldwide reach.

Aren’t we repeating past mistakes??

One of the most common comparisons we hear is that today’s market is eerily similar to the early 2000s, just before the dot-com bubble burst. The narrative goes like this: tech stocks have surged, valuations are stretched, and we are ignoring the warning signs of an imminent crash.

Now, I cannot guarantee that a market correction is not around the corner. History shows that bear markets are an unavoidable part of investing and show up randomly. They are a feature of the system, not a bug. However, a closer look at the data reveals clear differences between today and the dot-com bubble.

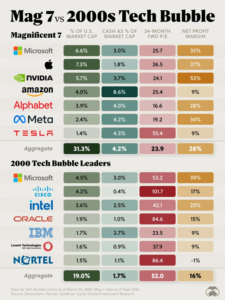

As shown in the chart below from Visual Capitalist, the dot-com era was driven by companies with sky-high valuations, much lower profit margins, and minimal cash reserves. In contrast, today’s Magnificent Seven are some of the most profitable businesses in history, generating enormous cash flows with forward P/E ratios far lower than those of 2000’s tech leaders, indicating much lower valuations.

The aggregate forward P/E ratio of the Magnificent Seven stood at 23.9 as of September 2024, compared to 52.0 during the dot-com era.

Cash reserves are also significantly higher, providing a buffer against economic downturns. But perhaps the most important factor of all is profitability. Companies like Nvidia now boast net profit margins above 50%.

The reality is that these companies are not speculative startups running on hype. They are cash-rich, structurally sound, and have built dominant positions in global industries. While volatility is inevitable, dismissing the current market as just another dot-com bubble ignores the fundamental strength of today’s tech giants.

What should we do to navigate this market environment?

Market corrections are a natural part of investing. They have always happened, and they always will. The idea that US equities are on the brink of collapse while the rest of the world stages a dramatic resurgence is simply not grounded in reality. Markets are constantly evolving, and a global market cap approach ensures that if US dominance declines, portfolios adjust naturally without the need for speculation or drastic repositioning.

The collective wisdom of global investors is reflected in a global market cap portfolio. This approach has stood the test of time, adapting as markets shift and capital moves to where it is most productive. It is a strategy built not on predictions or fleeting narratives, but on the simple reality that markets work.

History has shown that those who stay invested in a well-structured, globally diversified portfolio fare better than those who attempt to outguess the market. The temptation to react to every headline, every period of volatility, and every prediction of seismic change is strong, but ultimately unnecessary. The market has always been dynamic, and it will continue to be. What matters is having a portfolio that evolves with it, not against it.

The loudest voices may claim to see what is coming next, but investing is not about fortune-telling. It is about patience, discipline, and trust in a process that has been delivered time and again. Regardless of what Trump or Elon do next, their actions are just noise. Markets do not like the uncertainty some of that noise has generated, and volatility may remain higher for a while. But what truly drives asset prices over the long term is company fundamentals, not the latest headline. The real challenge is not surviving market corrections. It is resisting the urge to believe they require action.